A loan agreement, also known as a loan contract, is a document that outlines the financial agreement between a lender and a borrower. This legal instrument helps hold the borrower accountable to repay their business, personal, or student loan. A loan agreement template that includes all the requisite provisions is all you need to ensure that loan repayments are made accurately and on time.

How to sign a loan agreement template

Download the loan agreement template.

Replace the placeholder text with the details of your deal.

Click on the area of the agreement that needs to be signed.

Choose the type of signature you wish to include.

Include the name of the signer and date, if you wish.

Click Finish.

Contents of a loan agreement template

We suggest using Signeasy’s loan agreement template, then customizing it to include the lender’s desired terms.

Once completed and signed, it legally binds both the borrower and lender until the end of the contract term.

Here are some simple instructions on how to fill out Signeasy’s loan contract template:

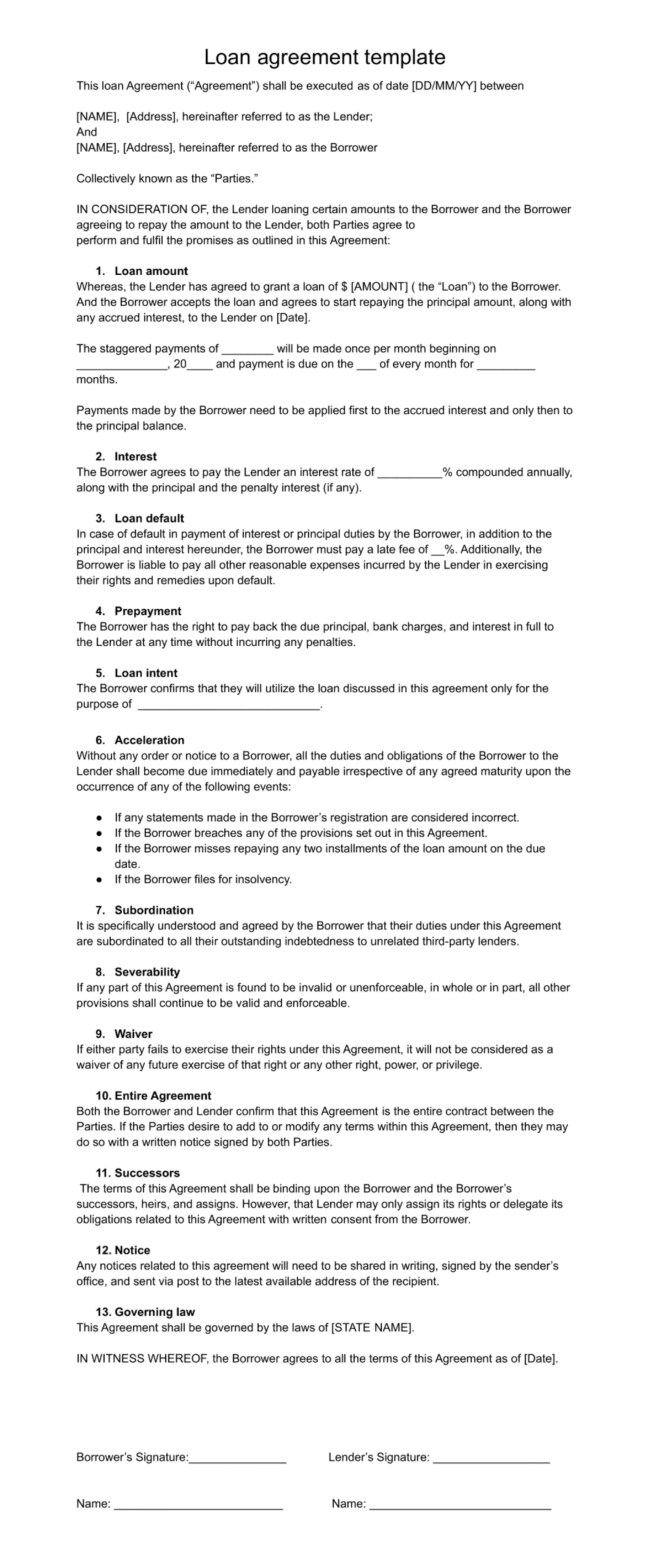

Introduction

In this section, you set the premise of the entire loan agreement. Start by identifying the lender and borrower, including the nature of their relationship.

Loan amount, repayment, and duration

How much money is the lender offering to the borrower? When will the borrower return the money along with interest? What is the payment plan for the loan? Answers to these questions and more are addressed in this clause.

Note: Sometimes the loan is paid back as a lump sum, and in other cases, it is repaid in installments.

Interest

This provision indicates the interest rate being charged by the lender that must be paid back by the borrower in addition to the principal.

Loan default

All loan installments and the associated interest must be paid within the time frame outlined in the agreement. If there is any delay in payment, you can specify the late fee that will be charged.

In this clause, you can also talk about who will be responsible for any legal charges expended by the lender in an effort to secure the defaulted payments.

Prepayment

This provision grants borrowers the right to pay back the loan and interest in full before the due date, and not incur any fines.

Acceleration

Sometimes, once a loan agreement has already been validated, the lender may come across reasons to doubt the borrower’s intent or ability to pay off the loan. In such cases, this provision demands that the borrower repays the entire remainder immediately. Some of the instances when this clause may be applicable are when the borrower:

Files for insolvency

Submits incorrect details during loan registration

Breaches the terms of this agreement

Does not pay two or more installments of the loan amount as per the schedule mentioned in this agreement

Boilerplate

Here are a number of legal provisions that are found across most contracts. These are the clauses that form the very foundation of the loan contract template:

Subordination: Prioritizes the clauses within this agreement over any prior agreements.

Severability: Ensures that even if a part of the agreement is found to be invalid, the rest of the agreement will still stand.

Waiver: Ensures that no part of the agreement will be considered waived in case the borrower or lender does not enforce its terms.

Entire agreement: Specifies that there are no further parts to this agreement and that modifications need to be made via written and signed notices.

Successors: That the borrower’s successors will be bound to the terms outlined in this agreement, if ever that becomes applicable. It also specifies that the lender can only assign its rights if the borrower also consents to the assignment.

Notice: Outlines the methods by which the lender and borrower may communicate with each other on matters related to this agreement.

Governing law: Specifies the jurisdiction that will govern the agreement.

Signature

Arguably the most important section of this contract, signatures formalize the terms and conditions of this document and make it legally binding.

To validate the agreement, it needs to be signed by both parties. Once it's signed by the borrower, the copy needs to be sent to the lender for their approval.

Since most paperwork is handled remotely nowadays, adopting an eSignature solution like Signeasy is the easiest way to smooth out your digital signing workflows.

Additional clauses to include in the loan contract template

Here are a few more clauses that are often included in a loan contract, along with the questions they help answer:

Collateral: Which physical asset belonging to the borrower can be kept as collateral in case they default on the payment?

Joint and several liability: Who is individually responsible for the repayment of the whole loan amount?

Right to transfer: Can the lender transfer the loan to a third party? If so, what are the terms?

Loan Agreement vs Promissory Note vs IOU

All three of these loan forms symbolize a promise by the borrower to repay the lender. The IOU is the least formal and most flexible document of the three. It is typically used for small amounts loaned to family and friends and is not legally binding.

On the other hand, the loan agreement and promissory note are more formal documents that outline the many steps and timelines for repayment. They offer greater protections to lenders.

A promissory note only requires the signature of the borrower, while a loan agreement requires signatures from both parties to make it legally binding. A loan agreement also outlines the consequences of defaulting.

Why draft a loan agreement?

When you want to hold a borrower liable for repaying the loan principal amount and interest on a given due date, you use a loan agreement.

In this document, you can mention terms of the payment installments and the interest to be levied. These loan contracts are typically used for:

Employee loans taken from an employer for various purposes

Personal loans that are offered to friends or family

If you are lending out money and want to keep the agreement above board, be sure to use our free loan contract template. Then, sign up for Signeasy’s 14-day free trial so that you may sign and send it to the borrower without ever meeting face-to-face or using archaic office supplies.

Note: These templates are provided for general informational purposes only and are not intended to constitute legal advice. We recommend consulting a qualified professional to ensure the template meets your specific needs and complies with applicable laws.

Frequently asked questions

Can I write my own loan agreement?

You can write your own loan document by including the loan principal amount, interest rates, payment schedules, and terms for acceleration of payment, late payment, prepayment, and boilerplate clauses. Or, you may simply use a loan agreement template. Additionally, it would be advisable to seek input from a lawyer to tailor the document to your needs.

How do you write a loan agreement form?

Introduce both parties, borrower and lender, and outline their relationship, Mention the agreement date, Outline the loan amount and payment schedule, Mention the interest levied, Mention late payment dues, Specify the terms for prepayment, Outline the terms for acceleration of payment, List all the boilerplate clauses such as entire agreement, waiver, notices, and governing law, Insert borrower’s and lender’s signature

What is a loan agreement?

Introduce both parties, borrower and lender, and outline their relationship, Mention the agreement date, Outline the loan amount and payment schedule, Mention the interest levied, Mention late payment dues, Specify the terms for prepayment, Outline the terms for acceleration of payment, List all the boilerplate clauses such as entire agreement, waiver, notices, and governing law, Insert borrower’s and lender’s signature

Does a loan agreement need to be witnessed?

Normally, it is not mandatory to have a witness or notary present when a loan agreement is signed. However, having a third party witness the act is better evidence if ever you need to enforce the agreement terms in court.